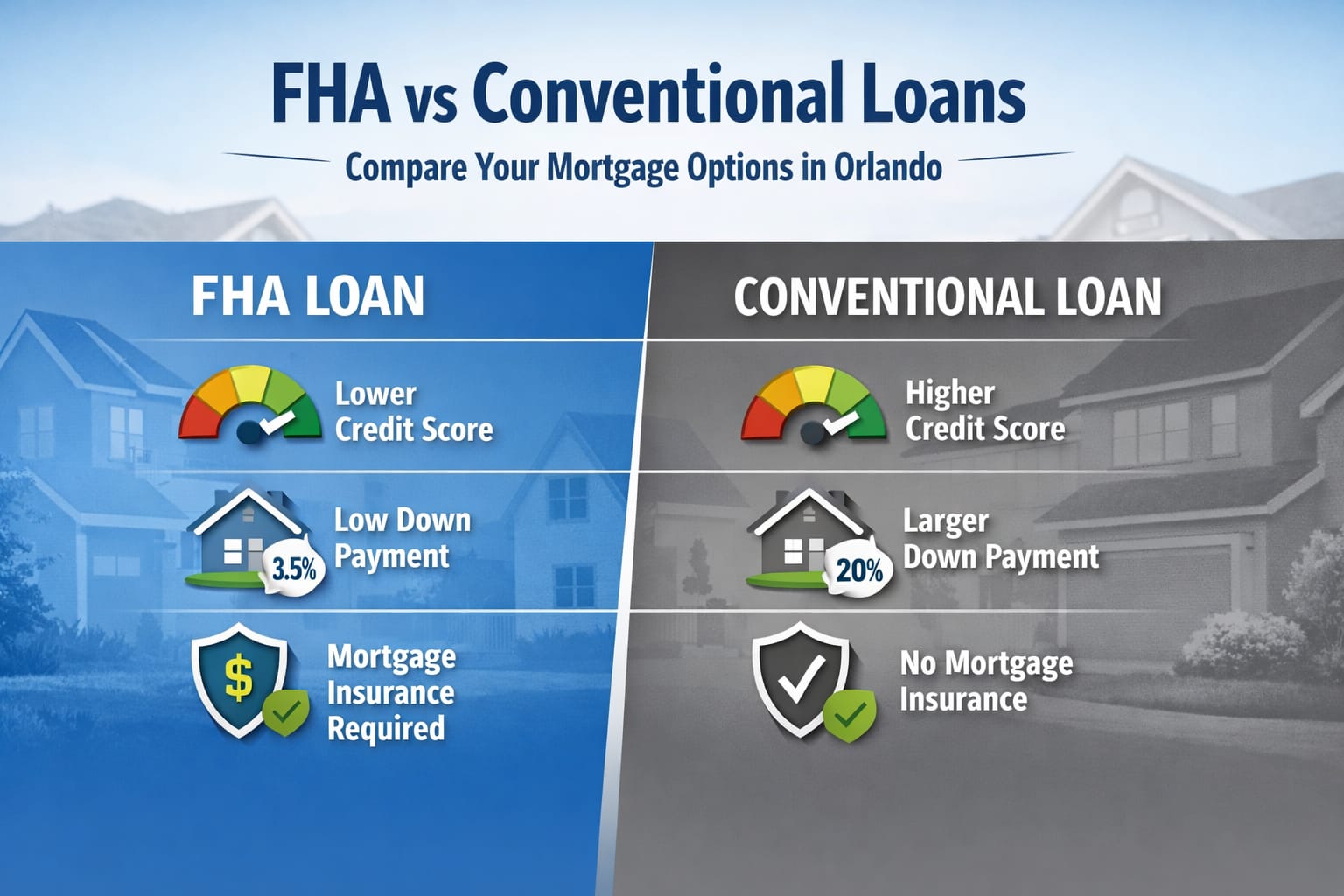

FHA vs Conventional Loans in Orlando: Which Is Better for First-Time Buyers?

Let's Keep In Touch!

New ORC Form Lead

"*" indicates required fields

"*" indicates required fields

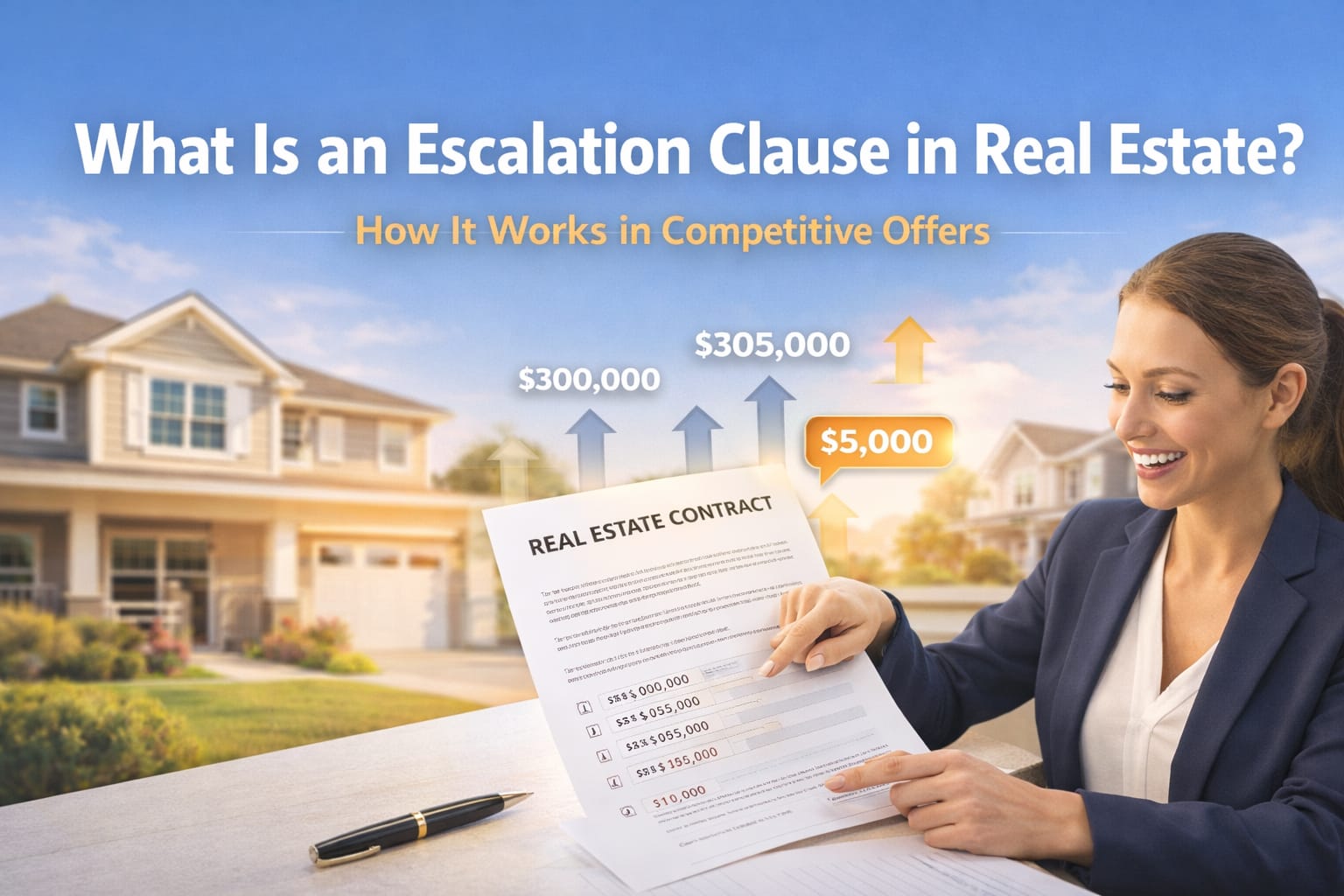

An escalation clause in real estate is a contract term that allows a buyer to automatically increase their offer price if the seller receives a higher competing offer, up to a maximum price set by the buyer.

If you’re buying a home in Orlando or Kissimmee, you’ve probably run into a multiple-offer situation. An escalation clause (sometimes called an escalation addendum or escalator clause) is a tool that can help you compete without immediately throwing out your highest number.

In plain English: an escalation clause lets your offer automatically increase if the seller receives a higher competing offer—up to a maximum price you choose. It can work well in a bidding war, but it also comes with real risks (especially appraisal issues) if it’s used carelessly.

If you’re earlier in the process, start here first: Orlando home buying guide and Kissimmee home buying tips.

An escalation clause is language in a purchase offer that includes:

Your offer: $400,000 with a $2,500 escalation up to $425,000.

Highest competing offer: $412,000.

Your escalated offer: $414,500 (beating it by $2,500).

| Item | What It Means | Why It Matters in Central Florida |

|---|---|---|

| Base Offer | Your starting price | Too low can get ignored in hot pockets of Orlando/Kissimmee |

| Escalation Amount | How much you outbid verified offers by | Helps you compete without guessing the exact “winning” number |

| Cap (Max Price) | Your ceiling | Protects your budget but can expose your top-end if handled poorly |

| Proof Requirement | What triggers the escalation | Prevents “phantom offer” concerns and reduces gamesmanship |

| Appraisal Risk | Home may not appraise at escalated price | One of the most common deal-breakers after bidding wars |

Escalation clauses are most useful when:

If you’re dealing with heavy competition, this pairs well with broader strategy: how to win a bidding war in Orlando.

If your offer escalates above recent comparable sales, the home may not appraise at the contract price. That can force you to:

Here’s a consumer-friendly explanation of appraisals from the CFPB: What is an appraisal?

If you want a local-focused explanation of how this plays out in competitive offers, add: appraisal gap explained.

Buyers often worry about an escalation clause being triggered without real competition. That’s why the offer should clearly define what counts as a bona fide competing offer and what proof is required.

In practice, proof language can vary. The point is simple: don’t leave this vague.

In many Orlando and Kissimmee listings, the seller will request “highest and best” by a deadline.

Either way, your offer has to be strong beyond price. If you’re still building your buyer profile (credit, savings, payment planning), these help:

For sellers, escalation clauses can be helpful—if the buyer is actually capable of closing at the escalated price.

Sellers should evaluate:

For additional consumer education on the homebuying process, Freddie Mac has a strong overview here: Freddie Mac My Home

No. Sellers can choose another offer with better terms, fewer contingencies, stronger financing, or a better closing timeline.

Only if your escalation clause requires it. If proof matters to you, it must be written clearly into the offer.

Yes. If the offer escalates above comparable sales, the appraisal may come in low and you’ll need a plan to handle the gap.

No. Use it when there’s real competition and the home is likely to appraise near your cap.

It depends. Sometimes a clean, strong offer upfront wins. Other times, escalation language helps you stay competitive without overpaying immediately.

It’s used in competitive situations, but not every seller or agent prefers them. Some listings will still push for “highest and best.”

Want help using an escalation clause the right way in Orlando or Kissimmee? We’ll review the comps, your cap, your financing strength, and the cleanest way to structure your offer so you’re competitive without creating avoidable problems.

Orlando Realty Consultants

Service Area: Central Florida

Se habla español.

Call or text: 407-902-7750

Also helpful as you prepare: home inspection checklist Florida and top 5 red flags when buying a home.

"*" indicates required fields

Selling your home as-is means you sell it in its current condition, without repairs, upgrades, or renovations. For homeowners facing foreclosure in Orlando and Central Florida, this is often the fastest and most realistic way to exit the property before the lender completes the foreclosure.

The goal is simple: sell before the foreclosure auction date. If done correctly, an as-is sale can stop foreclosure, reduce financial stress, and give you control over the outcome instead of letting the bank decide.

In many Orlando foreclosure cases, homeowners simply don’t have the time or money to prepare a home for the open market. As-is sales remove that barrier.

| Factor | Foreclosure | Sell As-Is |

|---|---|---|

| Credit Impact | Severe, long-term | Less damaging |

| Control | Lender controls outcome | You control the sale |

| Timeline | Forced and rigid | Flexible and faster |

| Repairs Required | None (bank owned) | None |

Florida is a judicial foreclosure state, which means the process can take months. That window creates opportunity. The earlier you act, the more options you have.

We evaluate value using recent MLS data, a professional Appraisal, or a lender-requested BPO, depending on your situation.

If your home is worth less than what you owe, a short sale may be required. I have extensive experience navigating the lender approvals, timelines, and documentation involved in the short sale process.

As-is homes attract investors, cash buyers, and renovation-ready buyers. The key is accurate positioning, clean disclosures, and aggressive timelines.

Foreclosure is stressful, but delay is the biggest enemy.

Orlando’s investor activity, strong rental demand, and population growth create real opportunities for distressed homeowners. Even homes needing major repairs often sell quickly when priced correctly.

I’ve helped homeowners across Orange, Osceola, Seminole, and Lake Counties sell as-is while facing foreclosure, liens, probate issues, and inherited property challenges.

At Orlando Realty Consultants, foreclosure and short sale work is not occasional — it’s a core specialty.

If you need a trusted Orlando short sale agent, you’re in the right place.

Yes. In most cases, you can sell until the foreclosure auction date.

If the sale closes before the auction, foreclosure is stopped.

No. Repairs are not required.

A short sale may be an option.

Some sell within days if priced correctly.

Often no, but lender approval terms matter.

Far less than a completed foreclosure.

Yes, those are handled during closing.

You can, but professional guidance helps avoid mistakes.

If you’re behind on payments or already facing foreclosure, time matters. The sooner you act, the more leverage you have.

Call Orlando Realty Consultants at 407-902-7750 for a confidential consultation. We’ll walk through your options honestly and help you decide the best path forward.

"*" indicates required fields

Thinking about selling your home? The questions you ask a realtor before listing can make the difference between selling quickly for top dollar — or sitting on the market and chasing price drops. The right agent should explain pricing, marketing, negotiations, and timing clearly, not dodge the tough questions.

Below is a practical, no-fluff guide to the most important questions to ask a realtor when selling, with specific insight into how this process works here in Orlando and Central Florida.

Selling a home isn’t just about putting a sign in the yard. It’s about pricing strategy, market timing, buyer demand, negotiation skill, and knowing how to handle problems when they come up.

Many sellers choose an agent based on a recommendation or a quick meeting — and later realize the agent wasn’t prepared to protect their bottom line. Asking the right questions upfront helps you avoid that mistake.

A strong answer should include recent comparable sales, local market trends, and buyer behavior — not just an automated estimate. Ask how they handle pricing in shifting markets and whether they factor in condition, upgrades, and demand.

Pricing isn’t “set it and forget it.” A good realtor should explain when to adjust price, how long to wait, and what signals they watch from buyers and showings.

Marketing should include professional photography, online exposure, syndication through MLS.com, and targeted buyer outreach — not just uploading the listing and hoping for the best.

Negotiation skill is where real money is won or lost. Ask how they handle multiple offers, inspection requests, appraisal gaps, and buyer concessions.

This is where experience matters. A knowledgeable agent understands the appraisal process and can challenge or negotiate when values don’t align. Learn more about how the Appraisal process works.

Not every offer is equal. Your realtor should verify financing, timelines, and buyer strength before advising you to accept an offer.

If you’re dealing with a short sale, foreclosure risk, or need to sell quickly, you want an agent who has handled these situations many times — not someone learning on your transaction.

You should know how frequently you’ll receive updates and whether communication is proactive or reactive.

| Strong Realtor | Weak Realtor |

|---|---|

| Explains pricing with real data | Suggests a price without support |

| Has a clear marketing plan | Relies only on MLS exposure |

| Experienced in negotiations | Avoids difficult conversations |

| Understands Orlando market nuances | Uses generic advice |

The Orlando market is unique. Neighborhood demand can change street by street. Investor activity, short-term rentals, and seasonal buyers all affect pricing and timing.

An experienced Realtor in Orlando understands how local inventory, insurance costs, HOA rules, and buyer financing trends impact your sale.

Some sellers want maximum price. Others need speed. If your goal is urgency — relocation, financial stress, or inherited property — your agent should clearly explain options to sell my house fast in Orlando without unrealistic promises.

Ask about pricing strategy, marketing, negotiation experience, communication, and local market knowledge.

At least two or three. Comparing answers helps reveal who is prepared and who isn’t.

While it’s possible to sell without one, most sellers benefit from pricing expertise, exposure, and negotiation skills.

It depends on price, condition, and market demand, but strategy matters more than timing.

An experienced agent can help you decide what to fix, what to leave, and how it affects price.

Yes — but only if they have real short sale experience. This is not an entry-level skill.

Avoid vague answers, unrealistic pricing, and agents who avoid hard conversations.

Read verified feedback and Check out my Google Reviews.

At Orlando Realty Consultants, I help sellers across Central Florida navigate traditional sales, fast sales, and complex short sale situations. I’ve worked with homeowners who needed speed, accuracy, and honest advice — not sales pressure.

If you’re thinking about selling and want clear answers, a realistic plan, and local expertise, let’s talk.

Call Orlando Realty Consultants at 407-902-7750

Serving Central Florida

Se habla Español

"*" indicates required fields

If you own a home in Orlando or Kissimmee and you want to buy your next home before you sell, you’re not alone. The problem is simple: most homeowners need their current equity for the down payment, but most sellers don’t love contingency offers.

A Buy Before You Sell program is designed to fix that gap. It helps you unlock your equity and purchase your next home first, then sell your current home afterward—usually with a lot less pressure and a lot more control.

This guide breaks down how these programs work, who they’re best for, what they cost, and what to watch out for—specifically for buyers and sellers in Central Florida.

A Buy Before You Sell program is a strategy (often supported by a lender or specialty company) that lets you:

These programs come in a few forms—some look like a bridge loan, some look like a guaranteed purchase / backup offer, and some are equity-advance models. The label “Buy Before You Sell” is the umbrella term.

For a national overview of how these programs are commonly structured, see: HomeLight’s explanation of Buy Before You Sell programs.

In Central Florida, a lot of people are trying to move without disrupting work, school, or childcare—and they don’t want to gamble on timing two closings perfectly. A Buy Before You Sell approach is popular here because it can:

If you’re also working on the “buying side” basics, this page can help: What credit score do you need to buy a house in Orlando?

Want to avoid buyer mistakes while you’re shopping? Read: Buying a home in Orlando: 5 red flags you shouldn’t ignore

A bridge loan is short-term financing that helps you access equity while your current home is on the market. It’s often used to cover the down payment on your next home and sometimes even pays off the first mortgage temporarily.

Learn how to evaluate loan options responsibly: CFPB mortgage resources

If you can qualify, a HELOC may allow you to pull equity for a down payment before you sell. This is often the “simplest” tool, but it depends heavily on credit, debt-to-income, and how quickly your lender can move.

These are programs offered by certain companies that help you buy first and then sell. Some provide a guaranteed offer on your current home, some provide an equity advance, and some coordinate financing and listing support together.

The biggest mistake I see is people focusing only on “Can I do it?” instead of “What will it cost me if I do it wrong?” Buy Before You Sell programs can absolutely be worth it—but the math needs to be honest.

Costs can include:

If you’re deciding whether to keep or sell a property (or turn it into a rental), you may also want: Is owning a short-term rental in Orlando still a good investment?

Want to estimate value and taxes locally? These county resources help: Orange County Property Appraiser and Osceola County Property Appraiser.

Yes—if you qualify financially. Many homeowners use bridge loans, HELOCs, or specialty Buy Before You Sell programs to access equity and make the purchase first.

Sometimes, yes—at least briefly. The whole point is to reduce pressure, but you still need a plan for overlap in case your current home takes longer to sell.

Often, yes. Removing (or reducing) a home-sale contingency typically makes your offer more attractive to sellers—especially in competitive areas.

It depends on the lender/provider and your debt-to-income. Start here for local guidance: Credit score requirements for buying in Orlando .

A bridge loan is one common tool used to buy before selling, but “Buy Before You Sell” can also include HELOCs and specialty provider programs.

The main risks are carrying two homes longer than expected, overestimating your sale price, and paying higher fees/interest if the timeline stretches.

Not necessarily. In many cases, buying first allows you to move out, then repair and present your home better—which can lead to a higher sale price. But you still need to budget for the work and timeline.

Program rules vary. Some give you a set window; others are more flexible. Your best move is choosing a structure that matches your realistic selling timeline.

It can be—especially if the program helps you win the right home and avoid moving twice. The key is running the numbers honestly (fees + overlap costs vs. convenience and stronger buying position).

Get a pricing and net sheet estimate for your current home, confirm your buying budget, and pick the best “buy first” structure for your situation. If you want help mapping this out, call 407-902-7750. Se Habla Español.

Buying before selling can be a smart move—but only when the financing, timeline, and pricing strategy are built correctly. If you want a clear plan for Orlando or Kissimmee (and you want someone to tell you the truth about the numbers), call 407-902-7750. Se Habla Español.

Helpful resources for buyers: National Association of REALTORS® | HUD home buying resources | IRS home sale capital gains basics

"*" indicates required fields