What Is an Escalation Clause in Real Estate? (Orlando & Kissimmee)

An escalation clause in real estate is a contract term that allows a buyer to automatically increase their offer price if the seller receives a higher competing offer, up to a maximum price set by the buyer.

- Base price: Your starting offer

- Escalation amount: How much you beat other offers by

- Price cap: The highest amount you’re willing to pay

If you’re buying a home in Orlando or Kissimmee, you’ve probably run into a multiple-offer situation. An escalation clause (sometimes called an escalation addendum or escalator clause) is a tool that can help you compete without immediately throwing out your highest number.

In plain English: an escalation clause lets your offer automatically increase if the seller receives a higher competing offer—up to a maximum price you choose. It can work well in a bidding war, but it also comes with real risks (especially appraisal issues) if it’s used carelessly.

If you’re earlier in the process, start here first: Orlando home buying guide and Kissimmee home buying tips.

Quick Definition (No Fluff)

An escalation clause is language in a purchase offer that includes:

- Base offer price (your starting offer)

- Escalation amount (how much you’ll beat a verified competing offer by)

- Maximum cap (your price ceiling)

- Trigger and proof requirements (what must happen—and what the seller must show—for the clause to activate)

How an Escalation Clause Works (Step-by-Step)

- You submit a base offer (example: $400,000).

- You set the escalation amount (example: “Buyer will beat any verified competing offer by $2,500”).

- You set a cap (example: “up to $425,000 maximum”).

- If a bona fide competing offer comes in, your offer increases only as much as needed—never above your cap.

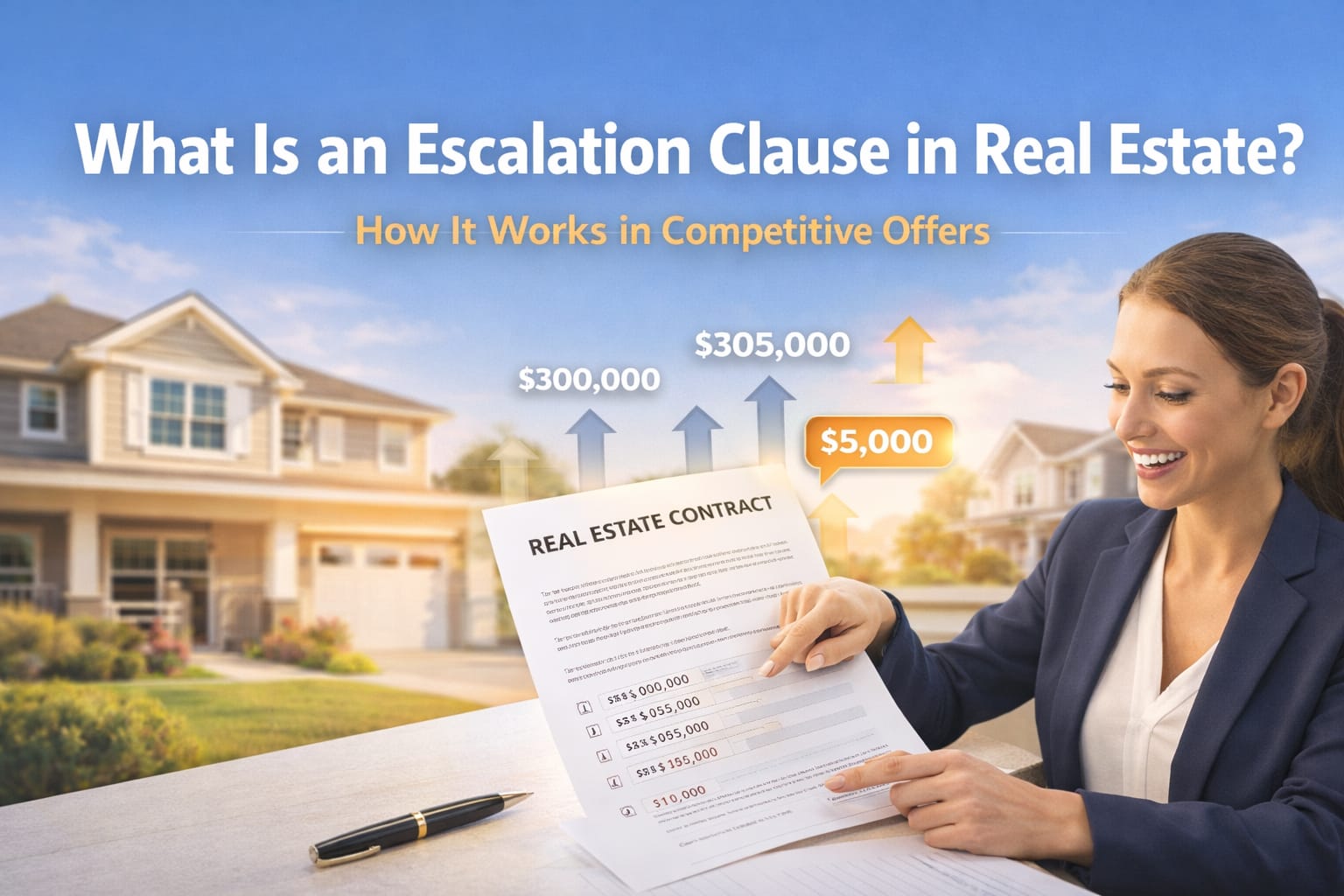

Real Example (With Numbers)

Your offer: $400,000 with a $2,500 escalation up to $425,000.

Highest competing offer: $412,000.

Your escalated offer: $414,500 (beating it by $2,500).

Escalation Clause Cheat Sheet

| Item | What It Means | Why It Matters in Central Florida |

|---|---|---|

| Base Offer | Your starting price | Too low can get ignored in hot pockets of Orlando/Kissimmee |

| Escalation Amount | How much you outbid verified offers by | Helps you compete without guessing the exact “winning” number |

| Cap (Max Price) | Your ceiling | Protects your budget but can expose your top-end if handled poorly |

| Proof Requirement | What triggers the escalation | Prevents “phantom offer” concerns and reduces gamesmanship |

| Appraisal Risk | Home may not appraise at escalated price | One of the most common deal-breakers after bidding wars |

When an Escalation Clause Makes Sense (Orlando & Kissimmee)

Escalation clauses are most useful when:

- You’re competing for a home that is clearly going to receive multiple offers.

- The asking price is close to market value and the home is likely to appraise.

- You want to remain competitive but keep a firm maximum purchase price.

- Your offer is strong on other terms (financing, timeline, clean paperwork).

If you’re dealing with heavy competition, this pairs well with broader strategy: how to win a bidding war in Orlando.

Pros and Cons (Honest Breakdown)

Pros for Buyers

- You may avoid overpaying upfront: your price only increases if there’s verified competition.

- You control the ceiling: the cap protects your budget.

- Stronger signal to sellers: shows you’re serious in a tight market.

Cons (What Can Go Wrong)

- You can expose your maximum: sellers may know your ceiling and negotiate accordingly.

- Appraisal gap risk: if the escalated price is above comps, the lender’s appraisal can come in low.

- Sellers may ignore it: some sellers prefer clean “highest and best” offers with no escalation language.

- It can complicate negotiations: more moving parts means more chances for misunderstandings.

The Biggest Risk: Appraisal Gap (Know This Before You Use One)

If your offer escalates above recent comparable sales, the home may not appraise at the contract price. That can force you to:

- bring additional cash to closing,

- renegotiate with the seller, or

- exit the deal if your contract terms allow it.

Here’s a consumer-friendly explanation of appraisals from the CFPB: What is an appraisal?

If you want a local-focused explanation of how this plays out in competitive offers, add: appraisal gap explained.

Proof of Competing Offer: Protect Yourself

Buyers often worry about an escalation clause being triggered without real competition. That’s why the offer should clearly define what counts as a bona fide competing offer and what proof is required.

In practice, proof language can vary. The point is simple: don’t leave this vague.

Escalation Clause vs. “Highest and Best”

In many Orlando and Kissimmee listings, the seller will request “highest and best” by a deadline.

- Highest and best: you submit your top number once; seller picks the strongest overall offer.

- Escalation clause: you start at a base price and increase only if needed, up to your cap.

Either way, your offer has to be strong beyond price. If you’re still building your buyer profile (credit, savings, payment planning), these help:

- What credit score do you need to buy a house in Orlando?

- Down payment assistance in Central Florida

- Florida closing costs guide

Best Practices (Buyer Checklist)

- Start with a realistic base offer (lowball offers often get ignored).

- Set a cap you can truly afford (payment, taxes, insurance, HOA if applicable).

- Pick a smart escalation amount (enough to matter, not so big you overpay).

- Require proof of a bona fide competing offer to trigger escalation.

- Plan for appraisal risk before you submit the offer.

- Keep the offer clean—timelines and documentation matter.

Seller Perspective: Should You Accept an Escalation Clause?

For sellers, escalation clauses can be helpful—if the buyer is actually capable of closing at the escalated price.

Sellers should evaluate:

- Financing strength: solid pre-approval, down payment, and underwriting reliability.

- Appraisal likelihood: will this turn into a price renegotiation later?

- Overall terms: inspection, timeline, and concessions affect your net proceeds.

For additional consumer education on the homebuying process, Freddie Mac has a strong overview here: Freddie Mac My Home

FAQs: Escalation Clauses in Real Estate

Do escalation clauses guarantee you’ll win the home?

No. Sellers can choose another offer with better terms, fewer contingencies, stronger financing, or a better closing timeline.

Do sellers have to show proof of the competing offer?

Only if your escalation clause requires it. If proof matters to you, it must be written clearly into the offer.

Can an escalation clause cause appraisal problems?

Yes. If the offer escalates above comparable sales, the appraisal may come in low and you’ll need a plan to handle the gap.

Should I use an escalation clause on every offer?

No. Use it when there’s real competition and the home is likely to appraise near your cap.

What’s better: escalation clause or raising my offer upfront?

It depends. Sometimes a clean, strong offer upfront wins. Other times, escalation language helps you stay competitive without overpaying immediately.

Is an escalation clause common in Florida?

It’s used in competitive situations, but not every seller or agent prefers them. Some listings will still push for “highest and best.”

Strong CTA: Get the Offer Strategy Right (Central Florida)

Want help using an escalation clause the right way in Orlando or Kissimmee? We’ll review the comps, your cap, your financing strength, and the cleanest way to structure your offer so you’re competitive without creating avoidable problems.

Orlando Realty Consultants

Service Area: Central Florida

Se habla español.

Call or text: 407-902-7750

Also helpful as you prepare: home inspection checklist Florida and top 5 red flags when buying a home.