If you’re thinking about buying your first home in Orlando or Kissimmee, you may be surprised by how many first-time home buyer programs are available in Florida. The key is knowing which programs actually help — and which ones sound good but don’t move the needle.

This guide breaks down the most common and useful first-time buyer programs and financing options so you can decide what works best for your situation.

If you want help matching the right program to your budget and credit, start here:

home

What Is Considered a First-Time Home Buyer?

In Florida, you’re typically considered a first-time home buyer if:

- You’ve never owned a home, or

- You haven’t owned a home in the last three years

Many buyers qualify even if they owned a home years ago.

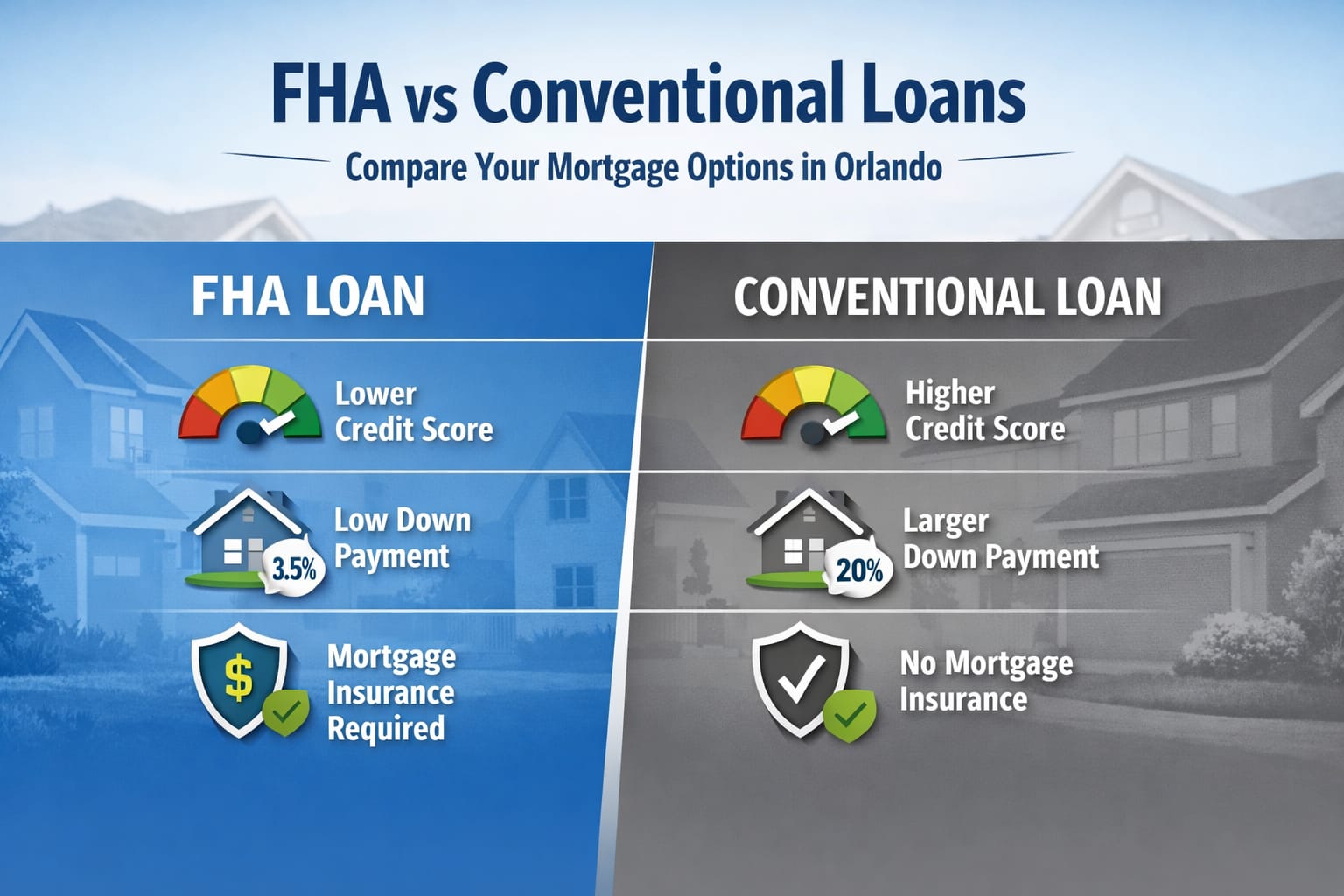

FHA Loans for First-Time Buyers

FHA loans are one of the most popular options for first-time buyers in Central Florida.

- Down payments as low as 3.5%

- More flexible credit requirements

- Allows higher debt-to-income ratios in many cases

FHA works well for buyers rebuilding credit or buying sooner rather than later.

Conventional First-Time Buyer Programs

Many buyers don’t realize that conventional loans can also work for first-time buyers.

- Down payments as low as 3% for qualified buyers

- Lower mortgage insurance costs with strong credit

- Mortgage insurance can be removed later

For a side-by-side comparison, see: FHA vs conventional loans in Orlando

Florida Down Payment Assistance Programs

Florida offers several statewide down payment assistance options depending on income, location, and loan type.

- Deferred second mortgages

- Forgivable assistance programs

- Low-interest assistance loans

Availability and requirements can change, so lender guidance is critical.

Orlando & Kissimmee Local Buyer Programs

Some city and county programs offer additional assistance for qualifying buyers in Orlando and Kissimmee.

- Income limits may apply

- Homebuyer education courses may be required

- Funds can be limited and competitive

These programs can help, but they are not instant approvals — timing and preparation matter.

Credit Score Requirements

Each program has different credit expectations:

- FHA programs may allow lower scores

- Conventional programs usually require stronger credit

- Down payment assistance programs often have overlays

For exact numbers, see: what credit score you need to buy a house in Orlando

How to Qualify for First-Time Buyer Programs

To improve your chances:

- Get pre-approved early

- Improve credit and reduce balances

- Complete any required homebuyer education

- Work with a Realtor who understands local programs

If you’re at the beginning of the process, start here: steps to buying a house for the first time

If credit is your biggest hurdle, this guide helps: how to build credit to buy a house

FAQs About First-Time Home Buyer Programs

Do first-time buyer programs really help?

Yes — when used correctly. They can reduce upfront costs, but they don’t replace good credit and solid planning.

Can I use multiple programs together?

Sometimes. Certain loans allow stacking assistance, but rules vary by lender and program.

Are these programs only for low-income buyers?

No. Many programs are income-based, but others are available to moderate-income buyers as well.

Want help choosing the right program? I’ll walk you through your options:

home